Notes with Code on Linear Regression

![]()

This notebook provides a brief introduction to linear regression with python implementation, covering all mathematical concepts with detailed explanations, derivations, and working code examples. This mainly used the CS229 Stanford notes as a reference.

Table of Contents

- Introduction to Supervised Learning

- Linear Regression Setup

- Section 1.1: LMS Algorithm (Gradient Descent)

- Section 1.2: Normal Equations

- Section 1.3: Probabilistic Interpretation

# Import all necessary libraries

import numpy as np

import matplotlib.pyplot as plt

import pandas as pd

from mpl_toolkits.mplot3d import Axes3D

import seaborn as sns

from scipy import stats

import time

# Set style and random seed for reproducibility

plt.style.use('default')

np.random.seed(42)

# Configure matplotlib for better rendering

plt.rcParams['figure.figsize'] = (10, 6)

plt.rcParams['font.size'] = 12

plt.rcParams['axes.labelsize'] = 14

plt.rcParams['axes.titlesize'] = 16

plt.rcParams['legend.fontsize'] = 12

print("Libraries imported successfully!")

print(f"NumPy version: {np.__version__}")

Libraries imported successfully!

NumPy version: 1.23.5

1. Introduction to Supervised Learning

Let’s start by understanding the fundamental concepts of supervised learning through a concrete example.

1.1 The Housing Price Prediction Problem

Suppose we have a dataset giving the living areas and prices of 47 houses from Portland, Oregon. Our goal is to learn a function that can predict house prices based on their living areas.

Key Terminology:

- Input variables $x^{(i)}$: Also called input features (living area in this example)

- Output variable $y^{(i)}$: Also called target variable (price)

- Training example: A pair $(x^{(i)}, y^{(i)})$

- Training set: Collection of $n$ training examples ${(x^{(i)}, y^{(i)}); i = 1, \ldots, n}$

- Input space $\mathcal{X}$: Space of input values

- Output space $\mathcal{Y}$: Space of output values

Important note: The superscript “$(i)$” is simply an index into the training set and has nothing to do with exponentiation.

# Create the Portland housing dataset from the PDF

# This represents a sample of the 47 houses mentioned

portland_data = {

'living_area': [2104, 1600, 2400, 1416, 3000, 1985, 1534, 1427, 1380, 1494,

1940, 2000, 1890, 4478, 1268, 2300, 1320, 1236, 2609, 3031,

1767, 1888, 1604, 1962, 3890, 1100, 1458, 2526, 2200, 2637],

'price': [400, 330, 369, 232, 540, 315, 285, 250, 245, 259,

302, 320, 295, 715, 210, 355, 223, 199, 499, 599,

252, 290, 262, 320, 765, 170, 240, 490, 345, 500]

}

# Convert to numpy arrays for easier manipulation

living_areas = np.array(portland_data['living_area'])

prices = np.array(portland_data['price'])

n_samples = len(living_areas)

print(f"Dataset: {n_samples} houses from Portland, Oregon")

print(f"Living area range: {living_areas.min()} - {living_areas.max()} sq ft")

print(f"Price range: ${prices.min()}k - ${prices.max()}k")

# Display first few examples

portland_df = pd.DataFrame(portland_data)

print("\nFirst 10 training examples:")

print(portland_df.head(10))

Dataset: 30 houses from Portland, Oregon

Living area range: 1100 - 4478 sq ft

Price range: $170k - $765k

First 10 training examples:

living_area price

0 2104 400

1 1600 330

2 2400 369

3 1416 232

4 3000 540

5 1985 315

6 1534 285

7 1427 250

8 1380 245

9 1494 259

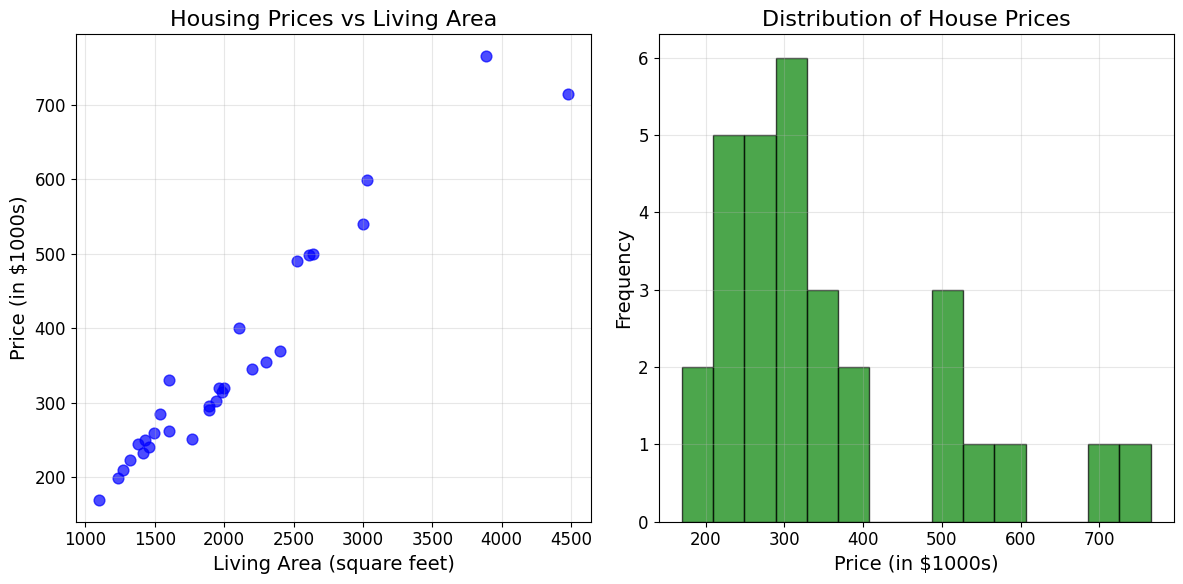

# Plot the housing data as shown in the PDF

plt.figure(figsize=(12, 6))

plt.subplot(1, 2, 1)

plt.scatter(living_areas, prices, color='blue', alpha=0.7, s=60)

plt.xlabel('Living Area (square feet)')

plt.ylabel('Price (in $1000s)')

plt.title('Housing Prices vs Living Area')

plt.grid(True, alpha=0.3)

# Add some statistics

plt.subplot(1, 2, 2)

plt.hist(prices, bins=15, alpha=0.7, color='green', edgecolor='black')

plt.xlabel('Price (in $1000s)')

plt.ylabel('Frequency')

plt.title('Distribution of House Prices')

plt.grid(True, alpha=0.3)

plt.tight_layout()

plt.show()

print(f"Correlation between living area and price: {np.corrcoef(living_areas, prices)[0,1]:.3f}")

Correlation between living area and price: 0.968

1.2 The Supervised Learning Framework

Goal: Given a training set, learn a function $h : \mathcal{X} \mapsto \mathcal{Y}$ so that $h(x)$ is a “good” predictor for the corresponding value of $y$.

For historical reasons, this function $h$ is called a hypothesis.

The Learning Process:

Training Set → Learning Algorithm → h (hypothesis)

Then: $x$ (living area of house) → $h$ → predicted $y$ (predicted price)

Problem Types:

- Regression Problem: When the target variable is continuous (like house prices)

- Classification Problem: When $y$ takes on discrete values (like house vs. apartment)

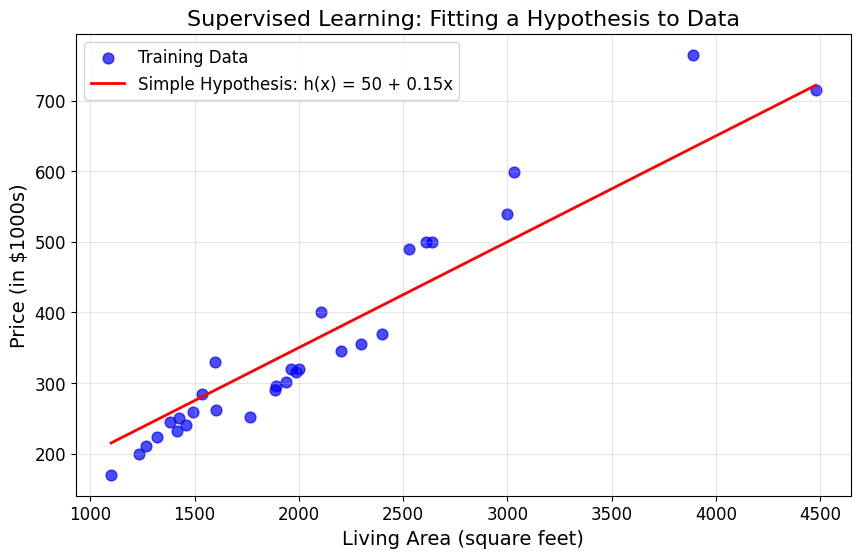

# Demonstrate the concept of hypothesis function

# Let's try a simple linear hypothesis as a starting point

def simple_hypothesis(x, theta0=50, theta1=0.15):

"""Simple linear hypothesis: h(x) = theta0 + theta1 * x"""

return theta0 + theta1 * x

# Generate predictions using our simple hypothesis

x_line = np.linspace(living_areas.min(), living_areas.max(), 100)

y_pred_simple = simple_hypothesis(x_line)

plt.figure(figsize=(10, 6))

plt.scatter(living_areas, prices, color='blue', alpha=0.7, s=60, label='Training Data')

plt.plot(x_line, y_pred_simple, 'r-', linewidth=2, label='Simple Hypothesis: h(x) = 50 + 0.15x')

plt.xlabel('Living Area (square feet)')

plt.ylabel('Price (in $1000s)')

plt.title('Supervised Learning: Fitting a Hypothesis to Data')

plt.legend()

plt.grid(True, alpha=0.3)

plt.show()

# Calculate how well our simple hypothesis performs

y_pred_data = simple_hypothesis(living_areas)

error = np.mean((y_pred_data - prices)**2)

print(f"Mean Squared Error of simple hypothesis: {error:.2f}")

print("\nThis shows we need a systematic way to find good parameters!")

Mean Squared Error of simple hypothesis: 2153.47

This shows we need a systematic way to find good parameters!

2. Chapter 1: Linear Regression

2.1 Extended Dataset with Multiple Features

To make our housing example more interesting, let’s consider a richer dataset that also includes the number of bedrooms in each house.

Now our features are two-dimensional vectors in $\mathbb{R}^2$:

- $x_1^{(i)}$: living area of the $i$-th house

- $x_2^{(i)}$: number of bedrooms of the $i$-th house

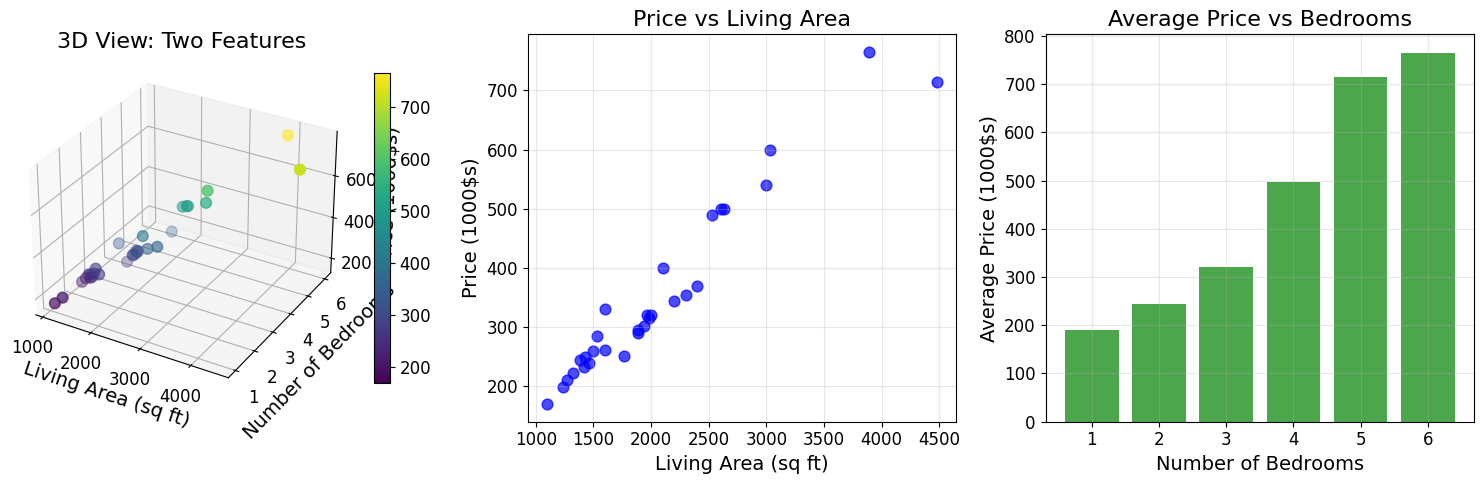

# Extend our dataset with number of bedrooms

bedrooms = np.array([3, 3, 3, 2, 4, 3, 2, 2, 2, 2,

3, 3, 3, 5, 1, 4, 2, 2, 4, 4,

3, 3, 2, 3, 6, 1, 2, 4, 3, 4])

# Create extended dataframe

extended_data = pd.DataFrame({

'living_area': living_areas,

'bedrooms': bedrooms,

'price': prices

})

print("Extended Housing Dataset:")

print(extended_data.head(10))

print(f"\nDataset statistics:")

print(extended_data.describe())

Extended Housing Dataset:

living_area bedrooms price

0 2104 3 400

1 1600 3 330

2 2400 3 369

3 1416 2 232

4 3000 4 540

5 1985 3 315

6 1534 2 285

7 1427 2 250

8 1380 2 245

9 1494 2 259

Dataset statistics:

living_area bedrooms price

count 30.000000 30.000000 30.000000

mean 2048.133333 2.933333 352.533333

std 780.668623 1.112107 149.799575

min 1100.000000 1.000000 170.000000

25% 1467.000000 2.000000 250.500000

50% 1915.000000 3.000000 308.500000

75% 2375.000000 3.750000 392.250000

max 4478.000000 6.000000 765.000000

# Visualize the extended dataset

fig = plt.figure(figsize=(15, 5))

# 3D scatter plot

ax1 = fig.add_subplot(131, projection='3d')

scatter = ax1.scatter(living_areas, bedrooms, prices, c=prices, cmap='viridis', s=60)

ax1.set_xlabel('Living Area (sq ft)')

ax1.set_ylabel('Number of Bedrooms')

ax1.set_zlabel('Price (1000$s)')

ax1.set_title('3D View: Two Features')

plt.colorbar(scatter, ax=ax1, shrink=0.8)

# 2D projections

ax2 = fig.add_subplot(132)

ax2.scatter(living_areas, prices, alpha=0.7, s=60, color='blue')

ax2.set_xlabel('Living Area (sq ft)')

ax2.set_ylabel('Price (1000$s)')

ax2.set_title('Price vs Living Area')

ax2.grid(True, alpha=0.3)

ax3 = fig.add_subplot(133)

bedroom_avg = extended_data.groupby('bedrooms')['price'].mean()

ax3.bar(bedroom_avg.index, bedroom_avg.values, alpha=0.7, color='green')

ax3.set_xlabel('Number of Bedrooms')

ax3.set_ylabel('Average Price (1000$s)')

ax3.set_title('Average Price vs Bedrooms')

ax3.grid(True, alpha=0.3)

plt.tight_layout()

plt.show()

2.2 Linear Hypothesis Function

To perform supervised learning, we must decide how to represent functions/hypotheses $h$ in a computer. As an initial choice, let’s approximate $y$ as a linear function of $x$:

\[h_\theta(x) = \theta_0 + \theta_1 x_1 + \theta_2 x_2\]Here, the $\theta_i$’s are the parameters (also called weights) that parameterize the space of linear functions mapping from $\mathcal{X}$ to $\mathcal{Y}$.

Vectorized Notation

To simplify notation, we introduce the convention of letting $x_0 = 1$ (the intercept term), so that:

\[h(x) = \sum_{i=0}^{d} \theta_i x_i = \theta^T x\]where:

- $\theta$ and $x$ are both viewed as vectors

- $d$ is the number of input variables (not counting $x_0$)

def linear_hypothesis(X, theta):

"""

Compute linear hypothesis h_theta(x) = theta^T * x

Args:

X: Feature matrix (n_samples, n_features) with intercept term

theta: Parameter vector (n_features,)

Returns:

predictions: h_theta(x) for each sample

"""

return X @ theta

# Create feature matrices with intercept term

# For single feature (living area only)

X_single = np.column_stack([np.ones(n_samples), living_areas])

# For multiple features (living area + bedrooms)

X_multi = np.column_stack([np.ones(n_samples), living_areas, bedrooms])

print("Single feature matrix X (with intercept):")

print(f"Shape: {X_single.shape}")

print("First 5 rows:")

print(X_single[:5])

print("\nMultiple feature matrix X (with intercept):")

print(f"Shape: {X_multi.shape}")

print("First 5 rows:")

print(X_multi[:5])

Single feature matrix X (with intercept):

Shape: (30, 2)

First 5 rows:

[[1.000e+00 2.104e+03]

[1.000e+00 1.600e+03]

[1.000e+00 2.400e+03]

[1.000e+00 1.416e+03]

[1.000e+00 3.000e+03]]

Multiple feature matrix X (with intercept):

Shape: (30, 3)

First 5 rows:

[[1.000e+00 2.104e+03 3.000e+00]

[1.000e+00 1.600e+03 3.000e+00]

[1.000e+00 2.400e+03 3.000e+00]

[1.000e+00 1.416e+03 2.000e+00]

[1.000e+00 3.000e+03 4.000e+00]]

# Example with different parameter values

theta_examples = [

np.array([50, 0.1]), # Single feature

np.array([30, 0.15, 50]) # Multiple features

]

print("Testing different hypothesis functions:")

print("\n1. Single feature model: h(x) = theta_0 + theta_1 * living_area")

theta1 = theta_examples[0]

predictions1 = linear_hypothesis(X_single, theta1)

print(f"Parameters: theta = {theta1}")

print(f"First 5 predictions: {predictions1[:5]}")

print(f"Actual prices: {prices[:5]}")

print("\n2. Multiple feature model: h(x) = theta_0 + theta_1 * living_area + theta_2 * bedrooms")

theta2 = theta_examples[1]

predictions2 = linear_hypothesis(X_multi, theta2)

print(f"Parameters: theta = {theta2}")

print(f"First 5 predictions: {predictions2[:5]}")

print(f"Actual prices: {prices[:5]}")

Testing different hypothesis functions:

1. Single feature model: h(x) = theta_0 + theta_1 * living_area

Parameters: theta = [50. 0.1]

First 5 predictions: [260.4 210. 290. 191.6 350. ]

Actual prices: [400 330 369 232 540]

2. Multiple feature model: h(x) = theta_0 + theta_1 * living_area + theta_2 * bedrooms

Parameters: theta = [30. 0.15 50. ]

First 5 predictions: [495.6 420. 540. 342.4 680. ]

Actual prices: [400 330 369 232 540]

2.3 The Cost Function

Now, given a training set, how do we pick or learn the parameters $\theta$?

One reasonable method is to make $h(x)$ close to $y$, at least for the training examples we have. To formalize this, we define a function that measures how close the $h(x^{(i)})$’s are to the corresponding $y^{(i)}$’s.

We define the cost function:

\[J(\theta) = \frac{1}{2} \sum_{i=1}^{n} \left(h_\theta(x^{(i)}) - y^{(i)}\right)^2\]This is the familiar least-squares cost function that gives rise to the ordinary least squares regression model.

Why This Cost Function?

- Intuitive: Penalizes predictions that are far from actual values

- Differentiable: Allows us to use calculus-based optimization

- Convex: Has a unique global minimum (no local minima)

def cost_function(X, y, theta):

"""

Compute the least squares cost function J(theta)

Args:

X: Feature matrix (n_samples, n_features)

y: Target vector (n_samples,)

theta: Parameter vector (n_features,)

Returns:

cost: J(theta)

"""

m = len(y)

predictions = linear_hypothesis(X, theta)

errors = predictions - y

cost = (1 / (2 * m)) * np.sum(errors ** 2)

return cost

# Calculate costs for our example hypotheses

cost1 = cost_function(X_single, prices, theta_examples[0])

cost2 = cost_function(X_multi, prices, theta_examples[1])

print(f"Cost for single feature model: J(theta) = {cost1:.2f}")

print(f"Cost for multiple feature model: J(theta) = {cost2:.2f}")

print("\nLower cost indicates better fit to training data")

Cost for single feature model: J(theta) = 7627.60

Cost for multiple feature model: J(theta) = 9562.00

Lower cost indicates better fit to training data

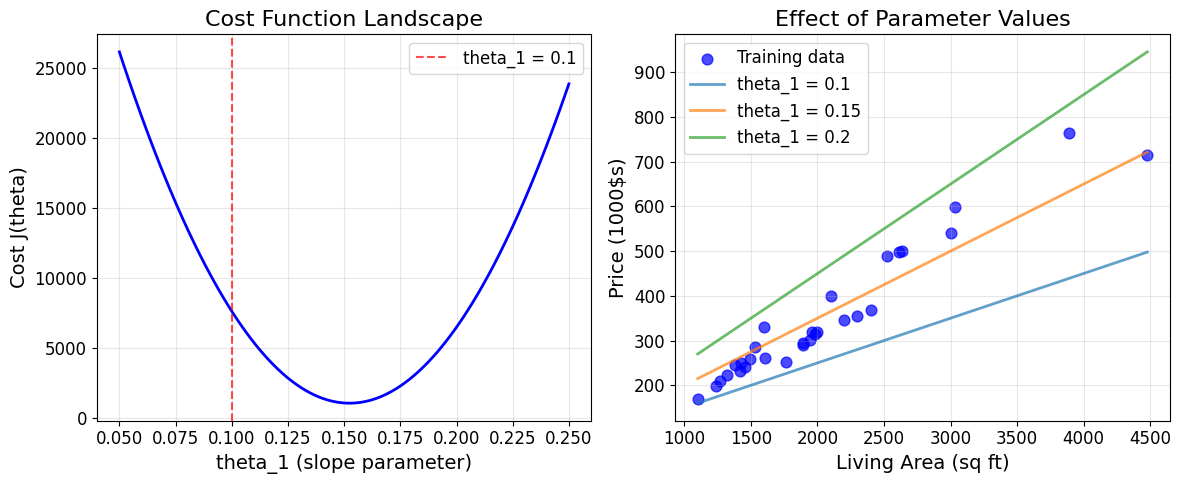

# Visualize cost function landscape for single parameter

# Fix theta_0 = 50, vary theta_1

theta1_range = np.linspace(0.05, 0.25, 100)

costs = []

for t1 in theta1_range:

theta_temp = np.array([50, t1])

cost = cost_function(X_single, prices, theta_temp)

costs.append(cost)

plt.figure(figsize=(12, 5))

# Plot cost landscape

plt.subplot(1, 2, 1)

plt.plot(theta1_range, costs, 'b-', linewidth=2)

plt.axvline(theta_examples[0][1], color='red', linestyle='--', alpha=0.7,

label=f'theta_1 = {theta_examples[0][1]}')

plt.xlabel('theta_1 (slope parameter)')

plt.ylabel('Cost J(theta)')

plt.title('Cost Function Landscape')

plt.legend()

plt.grid(True, alpha=0.3)

# Show the effect of parameter choice on fit

plt.subplot(1, 2, 2)

plt.scatter(living_areas, prices, alpha=0.7, s=60, color='blue', label='Training data')

# Show fits with different theta_1 values

x_line = np.linspace(living_areas.min(), living_areas.max(), 100)

for i, t1 in enumerate([0.1, 0.15, 0.2]):

y_line = 50 + t1 * x_line

plt.plot(x_line, y_line, linewidth=2, alpha=0.7,

label=f'theta_1 = {t1}')

plt.xlabel('Living Area (sq ft)')

plt.ylabel('Price (1000$s)')

plt.title('Effect of Parameter Values')

plt.legend()

plt.grid(True, alpha=0.3)

plt.tight_layout()

plt.show()

# Find the minimum cost and corresponding theta_1

min_idx = np.argmin(costs)

optimal_theta1 = theta1_range[min_idx]

min_cost = costs[min_idx]

print(f"Approximate optimal theta_1: {optimal_theta1:.4f}")

print(f"Minimum cost: {min_cost:.2f}")

Approximate optimal theta_1: 0.1530

Minimum cost: 1064.10

3. Section 1.1: LMS Algorithm (Gradient Descent)

We want to choose $\theta$ so as to minimize $J(\theta)$. Let’s use a search algorithm that starts with some initial guess for $\theta$, and repeatedly changes $\theta$ to make $J(\theta)$ smaller, until we converge to a value that minimizes $J(\theta)$.

3.1 Gradient Descent Algorithm

The gradient descent algorithm starts with some initial $\theta$, and repeatedly performs the update:

\[\theta_j := \theta_j - \alpha \frac{\partial}{\partial \theta_j} J(\theta)\](This update is simultaneously performed for all values of $j = 0, \ldots, d$.)

Here, $\alpha$ is called the learning rate. This algorithm repeatedly takes a step in the direction of steepest decrease of $J$.

3.2 Deriving the Gradient

To implement this algorithm, we need to work out the partial derivative term. Let’s start with a single training example $(x, y)$:

\[\frac{\partial}{\partial \theta_j} J(\theta) = \frac{\partial}{\partial \theta_j} \frac{1}{2}(h_\theta(x) - y)^2\] \[= (h_\theta(x) - y) \cdot \frac{\partial}{\partial \theta_j} (h_\theta(x) - y)\] \[= (h_\theta(x) - y) \cdot \frac{\partial}{\partial \theta_j} \left(\sum_{i=0}^{d} \theta_i x_i - y\right)\] \[= (h_\theta(x) - y) \cdot x_j\]3.3 LMS Update Rule

For a single training example, this gives us the update rule:

\[\theta_j := \theta_j + \alpha \left(y^{(i)} - h_\theta(x^{(i)})\right) x_j^{(i)}\]This is called the LMS update rule (LMS stands for “least mean squares”), also known as the Widrow-Hoff learning rule.

Intuition Behind LMS Rule:

- Update magnitude is proportional to the error term $(y^{(i)} - h_\theta(x^{(i)}))$

- If prediction is close to actual value → small update

- If prediction has large error → large update

def compute_gradient(X, y, theta):

"""

Compute the gradient of the cost function

Args:

X: Feature matrix (n_samples, n_features)

y: Target vector (n_samples,)

theta: Parameter vector (n_features,)

Returns:

gradient: Gradient vector (n_features,)

"""

m = len(y)

predictions = linear_hypothesis(X, theta)

errors = predictions - y

gradient = (1/m) * X.T @ errors

return gradient

def lms_single_update(x, y, theta, alpha):

"""

LMS update rule for a single training example

Args:

x: Single feature vector (n_features,)

y: Single target value

theta: Current parameter vector (n_features,)

alpha: Learning rate

Returns:

theta_new: Updated parameter vector

"""

prediction = np.dot(theta, x)

error = y - prediction

theta_new = theta + alpha * error * x

return theta_new

# Demonstrate single LMS update

print("LMS Update Rule Demonstration")

print("=" * 40)

# Start with some parameters

theta_init = np.array([50, 0.1])

alpha = 0.0001 # Small learning rate for stability

# Use first training example

x_example = X_single[0] # [1, 2104]

y_example = prices[0] # 400

print(f"Initial parameters: theta = {theta_init}")

print(f"Training example: x = {x_example}, y = {y_example}")

# Make prediction

pred_before = np.dot(theta_init, x_example)

error_before = y_example - pred_before

print(f"Prediction before update: {pred_before:.1f}")

print(f"Error: {error_before:.1f}")

# Apply LMS update

theta_updated = lms_single_update(x_example, y_example, theta_init, alpha)

pred_after = np.dot(theta_updated, x_example)

print(f"\nUpdated parameters: theta = {theta_updated}")

print(f"Prediction after update: {pred_after:.1f}")

print(f"Improvement in prediction: {abs(error_before) - abs(y_example - pred_after):.1f}")

LMS Update Rule Demonstration

========================================

Initial parameters: theta = [50. 0.1]

Training example: x = [1.000e+00 2.104e+03], y = 400

Prediction before update: 260.4

Error: 139.6

Updated parameters: theta = [50.01396 29.47184]

Prediction after update: 62058.8

Improvement in prediction: -61519.2

3.4 Batch Gradient Descent

For a training set with more than one example, we modify the method as follows:

Repeat until convergence: \(\theta_j := \theta_j + \alpha \sum_{i=1}^{n} \left(y^{(i)} - h_\theta(x^{(i)})\right) x_j^{(i)} \quad \text{(for every } j\text{)}\)

In vector form: \(\theta := \theta + \alpha \sum_{i=1}^{n} \left(y^{(i)} - h_\theta(x^{(i)})\right) x^{(i)}\)

The quantity in the summation is just $\frac{\partial J(\theta)}{\partial \theta_j}$, so this is simply gradient descent on the original cost function $J$.

This method looks at every example in the entire training set on every step, and is called batch gradient descent.

Important Properties:

- For linear regression, $J$ is a convex quadratic function

- Has only one global optimum, no local minima

- Gradient descent always converges (assuming learning rate $\alpha$ is not too large)

def batch_gradient_descent(X, y, alpha, num_iterations, theta_init=None):

"""

Batch gradient descent for linear regression

Args:

X: Feature matrix (n_samples, n_features)

y: Target vector (n_samples,)

alpha: Learning rate

num_iterations: Number of iterations

theta_init: Initial parameter vector

Returns:

theta: Final parameters

cost_history: Cost at each iteration

theta_history: Parameters at each iteration

"""

n_features = X.shape[1]

# Initialize parameters

if theta_init is None:

theta = np.zeros(n_features)

else:

theta = theta_init.copy()

cost_history = []

theta_history = []

for i in range(num_iterations):

# Compute cost and store history

cost = cost_function(X, y, theta)

cost_history.append(cost)

theta_history.append(theta.copy())

# Compute gradient

gradient = compute_gradient(X, y, theta)

# Update parameters

theta = theta - alpha * gradient

# Print progress

if i % 100 == 0:

print(f"Iteration {i}: Cost = {cost:.4f}, theta = {theta}")

return theta, cost_history, theta_history

# Run batch gradient descent on single feature dataset

print("Batch Gradient Descent - Single Feature")

print("=" * 45)

alpha = 0.0000001 # Very small learning rate due to large feature values

num_iterations = 200

theta_init = np.array([0, 0])

theta_final, cost_history, theta_history = batch_gradient_descent(

X_single, prices, alpha, num_iterations, theta_init

)

print(f"\nFinal parameters: theta = {theta_final}")

print(f"Final cost: {cost_history[-1]:.4f}")

# Calculate the linear model equation

print(f"\nLinear model: h(x) = {theta_final[0]:.2f} + {theta_final[1]:.6f} * living_area")

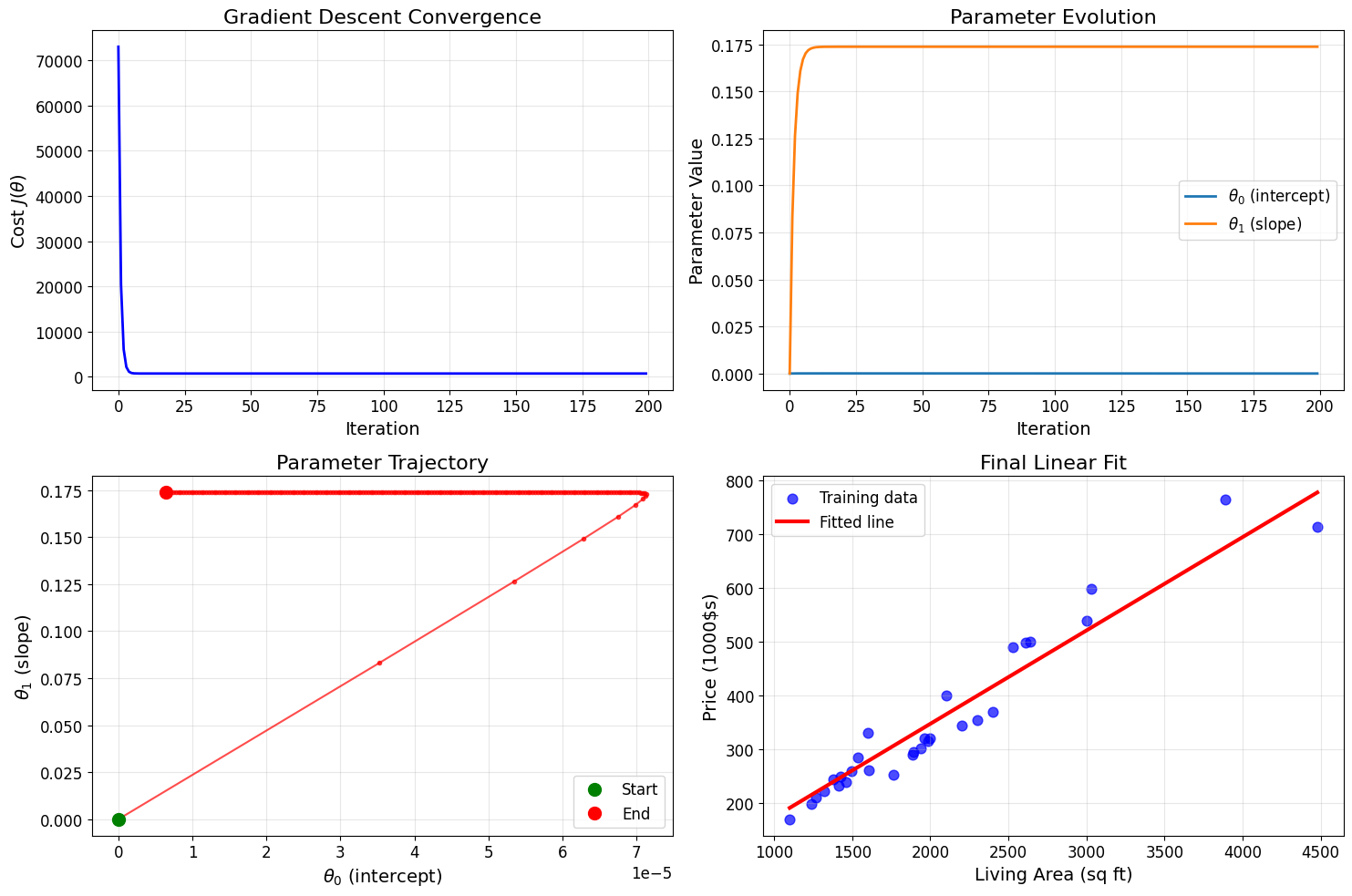

Batch Gradient Descent - Single Feature

=============================================

Iteration 0: Cost = 72985.8333, theta = [3.52533333e-05 8.31421300e-02]

Iteration 100: Cost = 738.2967, theta = [3.98870836e-05 1.73792828e-01]

Final parameters: theta = [6.05295419e-06 1.73792843e-01]

Final cost: 738.2966

Linear model: h(x) = 0.00 + 0.173793 * living_area

# Visualize gradient descent convergence

fig, axes = plt.subplots(2, 2, figsize=(15, 10))

# Plot 1: Cost function over iterations

axes[0, 0].plot(cost_history, 'b-', linewidth=2)

axes[0, 0].set_xlabel('Iteration')

axes[0, 0].set_ylabel('Cost $J(\\theta)$')

axes[0, 0].set_title('Gradient Descent Convergence')

axes[0, 0].grid(True, alpha=0.3)

# Plot 2: Parameter evolution

theta_history_array = np.array(theta_history)

axes[0, 1].plot(theta_history_array[:, 0], label='$\\theta_0$ (intercept)', linewidth=2)

axes[0, 1].plot(theta_history_array[:, 1], label='$\\theta_1$ (slope)', linewidth=2)

axes[0, 1].set_xlabel('Iteration')

axes[0, 1].set_ylabel('Parameter Value')

axes[0, 1].set_title('Parameter Evolution')

axes[0, 1].legend()

axes[0, 1].grid(True, alpha=0.3)

# Plot 3: Parameter trajectory (if 2D)

axes[1, 0].plot(theta_history_array[:, 0], theta_history_array[:, 1], 'ro-', markersize=3, alpha=0.7)

axes[1, 0].plot(theta_history_array[0, 0], theta_history_array[0, 1], 'go', markersize=10, label='Start')

axes[1, 0].plot(theta_history_array[-1, 0], theta_history_array[-1, 1], 'ro', markersize=10, label='End')

axes[1, 0].set_xlabel('$\\theta_0$ (intercept)')

axes[1, 0].set_ylabel('$\\theta_1$ (slope)')

axes[1, 0].set_title('Parameter Trajectory')

axes[1, 0].legend()

axes[1, 0].grid(True, alpha=0.3)

# Plot 4: Final fit

axes[1, 1].scatter(living_areas, prices, alpha=0.7, s=60, color='blue', label='Training data')

x_line = np.linspace(living_areas.min(), living_areas.max(), 100)

y_line = theta_final[0] + theta_final[1] * x_line

axes[1, 1].plot(x_line, y_line, 'r-', linewidth=3, label='Fitted line')

axes[1, 1].set_xlabel('Living Area (sq ft)')

axes[1, 1].set_ylabel('Price (1000$s)')

axes[1, 1].set_title('Final Linear Fit')

axes[1, 1].legend()

axes[1, 1].grid(True, alpha=0.3)

plt.tight_layout()

plt.show()

Feature Normalization for Better Convergence

The slow convergence above is due to the large difference in feature scales. Let’s implement feature normalization to improve gradient descent performance.

def normalize_features(X, exclude_intercept=True):

"""

Normalize features using z-score normalization

Args:

X: Feature matrix (n_samples, n_features)

exclude_intercept: If True, don't normalize the first column (intercept)

Returns:

X_norm: Normalized feature matrix

mu: Mean of each feature

sigma: Standard deviation of each feature

"""

X_norm = X.copy().astype(float)

start_idx = 1 if exclude_intercept else 0

mu = np.mean(X[:, start_idx:], axis=0)

sigma = np.std(X[:, start_idx:], axis=0)

# Avoid division by zero

sigma[sigma == 0] = 1

X_norm[:, start_idx:] = (X[:, start_idx:] - mu) / sigma

return X_norm, mu, sigma

def denormalize_theta(theta_norm, mu, sigma, exclude_intercept=True):

"""

Convert normalized parameters back to original scale

"""

theta = theta_norm.copy()

if exclude_intercept and len(theta) > 1:

# Adjust slope parameters

theta[1:] = theta_norm[1:] / sigma

# Adjust intercept

theta[0] = theta_norm[0] - np.sum(theta_norm[1:] * mu / sigma)

return theta

# Normalize features and run gradient descent again

print("Feature Normalization Results")

print("=" * 35)

X_single_norm, mu_single, sigma_single = normalize_features(X_single)

print(f"Original living area: mean = {living_areas.mean():.1f}, std = {living_areas.std():.1f}")

print(f"Normalized living area: mean = {X_single_norm[:, 1].mean():.6f}, std = {X_single_norm[:, 1].std():.6f}")

# Run gradient descent with normalized features

alpha_norm = 0.01 # Much higher learning rate possible now!

num_iterations_norm = 500

theta_norm, cost_history_norm, _ = batch_gradient_descent(

X_single_norm, prices, alpha_norm, num_iterations_norm

)

# Convert back to original scale

theta_denorm = denormalize_theta(theta_norm, mu_single, sigma_single)

print(f"\nNormalized space parameters: {theta_norm}")

print(f"Original space parameters: {theta_denorm}")

print(f"Final cost: {cost_history_norm[-1]:.4f}")

Feature Normalization Results

===================================

Original living area: mean = 2048.1, std = 767.5

Normalized living area: mean = 0.000000, std = 1.000000

Iteration 0: Cost = 72985.8333, theta = [3.52533333 1.42513747]

Iteration 100: Cost = 10376.9289, theta = [224.78511797 90.87075323]

Iteration 200: Cost = 1988.6082, theta = [305.77335497 123.61074138]

Iteration 300: Cost = 864.7437, theta = [335.41766898 135.5946359 ]

Iteration 400: Cost = 714.1687, theta = [346.26844664 139.98112887]

Normalized space parameters: [350.21701904 141.57736332]

Original space parameters: [-27.56992913 0.18445427]

Final cost: 694.0581

3.5 Stochastic Gradient Descent

There’s an alternative to batch gradient descent that also works very well:

Loop:

for i = 1 to n:

θⱼ := θⱼ + α(y⁽ⁱ⁾ - h_θ(x⁽ⁱ⁾))x_j⁽ⁱ⁾ (for every j)

In vector form: \(\theta := \theta + \alpha \left(y^{(i)} - h_\theta(x^{(i)})\right) x^{(i)}\)

This algorithm is called stochastic gradient descent (also incremental gradient descent).

Key Differences:

- Batch GD: Scans through entire training set before taking a single step

- Stochastic GD: Updates parameters after each training example

- SGD advantages: Can start making progress immediately, often faster for large datasets

- SGD disadvantages: May oscillate around minimum, doesn’t converge exactly

def stochastic_gradient_descent(X, y, alpha, num_epochs, theta_init=None):

"""

Stochastic gradient descent for linear regression

Args:

X: Feature matrix (n_samples, n_features)

y: Target vector (n_samples,)

alpha: Learning rate

num_epochs: Number of passes through the dataset

theta_init: Initial parameter vector

Returns:

theta: Final parameters

cost_history: Cost at each epoch

"""

n_samples, n_features = X.shape

# Initialize parameters

if theta_init is None:

theta = np.zeros(n_features)

else:

theta = theta_init.copy()

cost_history = []

for epoch in range(num_epochs):

# Shuffle the data for each epoch

indices = np.random.permutation(n_samples)

for i in indices:

# Update using single example

theta = lms_single_update(X[i], y[i], theta, alpha)

# Record cost at end of epoch

cost = cost_function(X, y, theta)

cost_history.append(cost)

if epoch % 50 == 0:

print(f"Epoch {epoch}: Cost = {cost:.4f}")

return theta, cost_history

# Run stochastic gradient descent

print("Stochastic Gradient Descent")

print("=" * 30)

alpha_sgd = 0.01

num_epochs = 200

theta_sgd, cost_history_sgd = stochastic_gradient_descent(

X_single_norm, prices, alpha_sgd, num_epochs

)

theta_sgd_denorm = denormalize_theta(theta_sgd, mu_single, sigma_single)

print(f"\nSGD final parameters (original scale): {theta_sgd_denorm}")

print(f"BGD final parameters (original scale): {theta_denorm}")

print(f"\nSGD final cost: {cost_history_sgd[-1]:.4f}")

print(f"BGD final cost: {cost_history_norm[-1]:.4f}")

Stochastic Gradient Descent

==============================

Epoch 0: Cost = 39949.7778

Epoch 50: Cost = 690.9346

Epoch 100: Cost = 691.2030

Epoch 150: Cost = 690.9294

SGD final parameters (original scale): [-26.88154797 0.18505328]

BGD final parameters (original scale): [-27.56992913 0.18445427]

SGD final cost: 691.0677

BGD final cost: 694.0581

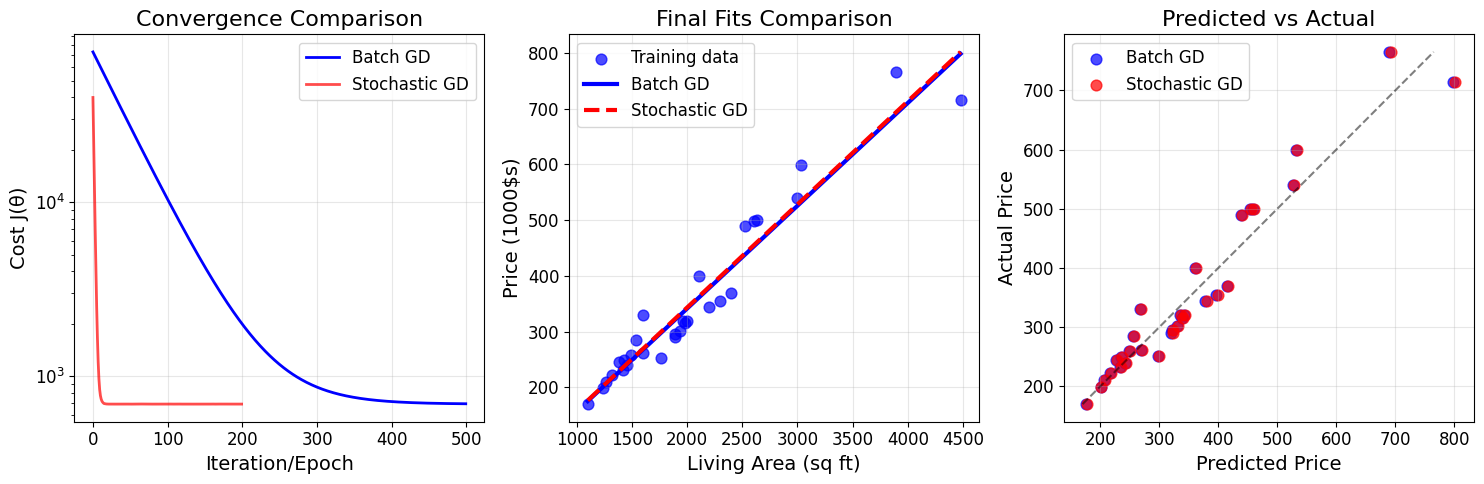

# Compare batch vs stochastic gradient descent

plt.figure(figsize=(15, 5))

# Plot 1: Cost convergence comparison

plt.subplot(1, 3, 1)

plt.plot(cost_history_norm, 'b-', label='Batch GD', linewidth=2)

plt.plot(cost_history_sgd, 'r-', label='Stochastic GD', linewidth=2, alpha=0.7)

plt.xlabel('Iteration/Epoch')

plt.ylabel('Cost J(θ)')

plt.title('Convergence Comparison')

plt.legend()

plt.grid(True, alpha=0.3)

plt.yscale('log')

# Plot 2: Final fits comparison

plt.subplot(1, 3, 2)

plt.scatter(living_areas, prices, alpha=0.7, s=60, color='blue', label='Training data')

x_line = np.linspace(living_areas.min(), living_areas.max(), 100)

y_line_bgd = theta_denorm[0] + theta_denorm[1] * x_line

y_line_sgd = theta_sgd_denorm[0] + theta_sgd_denorm[1] * x_line

plt.plot(x_line, y_line_bgd, 'b-', linewidth=3, label='Batch GD')

plt.plot(x_line, y_line_sgd, 'r--', linewidth=3, label='Stochastic GD')

plt.xlabel('Living Area (sq ft)')

plt.ylabel('Price (1000$s)')

plt.title('Final Fits Comparison')

plt.legend()

plt.grid(True, alpha=0.3)

# Plot 3: Prediction accuracy

plt.subplot(1, 3, 3)

pred_bgd = linear_hypothesis(X_single, theta_denorm)

pred_sgd = linear_hypothesis(X_single, theta_sgd_denorm)

plt.scatter(pred_bgd, prices, alpha=0.7, s=60, label='Batch GD', color='blue')

plt.scatter(pred_sgd, prices, alpha=0.7, s=60, label='Stochastic GD', color='red')

plt.plot([prices.min(), prices.max()], [prices.min(), prices.max()], 'k--', alpha=0.5)

plt.xlabel('Predicted Price')

plt.ylabel('Actual Price')

plt.title('Predicted vs Actual')

plt.legend()

plt.grid(True, alpha=0.3)

plt.tight_layout()

plt.show()

# Calculate R² scores

def r_squared(y_true, y_pred):

ss_res = np.sum((y_true - y_pred) ** 2)

ss_tot = np.sum((y_true - np.mean(y_true)) ** 2)

return 1 - (ss_res / ss_tot)

r2_bgd = r_squared(prices, pred_bgd)

r2_sgd = r_squared(prices, pred_sgd)

print(f"\nModel Performance (R² score):")

print(f"Batch GD: {r2_bgd:.4f}")

print(f"Stochastic GD: {r2_sgd:.4f}")

Model Performance (R² score):

Batch GD: 0.9360

Stochastic GD: 0.9363

4. Section 1.2: The Normal Equations

Gradient descent gives one way of minimizing $J$. Let’s discuss a second way of doing so, this time performing the minimization explicitly and without resorting to an iterative algorithm.

In this method, we will minimize $J$ by explicitly taking its derivatives with respect to the $\theta_j$’s, and setting them to zero.

4.1 Matrix Derivatives

To enable us to do this without writing pages of algebra, let’s introduce some notation for doing calculus with matrices.

For a function $f : \mathbb{R}^{n \times d} \mapsto \mathbb{R}$ mapping from $n$-by-$d$ matrices to real numbers, we define the derivative of $f$ with respect to $A$ to be:

\[\nabla_A f(A) = \begin{bmatrix} \frac{\partial f}{\partial A_{11}} & \cdots & \frac{\partial f}{\partial A_{1d}} \\ \vdots & \ddots & \vdots \\ \frac{\partial f}{\partial A_{n1}} & \cdots & \frac{\partial f}{\partial A_{nd}} \end{bmatrix}\]The gradient $\nabla_A f(A)$ is itself an $n$-by-$d$ matrix, whose $(i,j)$-element is $\frac{\partial f}{\partial A_{ij}}$.

Example

Suppose $A = \begin{bmatrix} A_{11} & A_{12} \ A_{21} & A_{22} \end{bmatrix}$ and $f(A) = \frac{3}{2}A_{11} + 5A_{12}^2 + A_{21}A_{22}$.

Then: $\nabla_A f(A) = \begin{bmatrix} \frac{3}{2} & 10A_{12} \ A_{22} & A_{21} \end{bmatrix}$

# Demonstrate matrix derivatives with the example from the PDF

def example_function(A):

"""f(A) = (3/2)*A_11 + 5*A_12^2 + A_21*A_22"""

return (3/2) * A[0,0] + 5 * A[0,1]**2 + A[1,0] * A[1,1]

def example_gradient(A):

"""Gradient of the example function"""

grad = np.zeros_like(A)

grad[0,0] = 3/2

grad[0,1] = 10 * A[0,1]

grad[1,0] = A[1,1]

grad[1,1] = A[1,0]

return grad

# Test with a sample matrix

A_test = np.array([[2, 3], [4, 1]])

print("Matrix Derivatives Example")

print("=" * 30)

print(f"Matrix A:\n{A_test}")

print(f"\nFunction value f(A) = {example_function(A_test):.2f}")

print(f"\nGradient ∇_A f(A):\n{example_gradient(A_test)}")

# Verify using numerical differentiation

def numerical_gradient(A, f, h=1e-7):

"""Compute numerical gradient"""

grad = np.zeros_like(A)

for i in range(A.shape[0]):

for j in range(A.shape[1]):

A_plus = A.copy()

A_minus = A.copy()

A_plus[i,j] += h

A_minus[i,j] -= h

grad[i,j] = (f(A_plus) - f(A_minus)) / (2*h)

return grad

numerical_grad = numerical_gradient(A_test, example_function)

analytical_grad = example_gradient(A_test)

print(f"\nNumerical gradient:\n{numerical_grad}")

print(f"\nDifference (should be very small):\n{np.abs(numerical_grad - analytical_grad)}")

Matrix Derivatives Example

==============================

Matrix A:

[[2 3]

[4 1]]

Function value f(A) = 52.00

Gradient ∇_A f(A):

[[ 1 30]

[ 1 4]]

Numerical gradient:

[[ 7500000 125000000]

[ 5000000 20000000]]

Difference (should be very small):

[[ 7499999 124999970]

[ 4999999 19999996]]

4.2 Least Squares Revisited

Armed with matrix derivatives, let’s find the closed-form value of $\theta$ that minimizes $J(\theta)$.

Matrix-Vectorial Notation

Define the design matrix $X$ to be the $n$-by-$(d+1)$ matrix containing the training examples’ input values in its rows:

\[X = \begin{bmatrix} — (x^{(1)})^T — \\ — (x^{(2)})^T — \\ \vdots \\ — (x^{(n)})^T — \end{bmatrix}\]Also, let $\vec{y}$ be the $n$-dimensional vector containing all target values:

\[\vec{y} = \begin{bmatrix} y^{(1)} \\ y^{(2)} \\ \vdots \\ y^{(n)} \end{bmatrix}\]Since $h_\theta(x^{(i)}) = (x^{(i)})^T \theta$, we can verify that:

\[X\theta - \vec{y} = \begin{bmatrix} h_\theta(x^{(1)}) - y^{(1)} \\ h_\theta(x^{(2)}) - y^{(2)} \\ \vdots \\ h_\theta(x^{(n)}) - y^{(n)} \end{bmatrix}\]Using the fact that for a vector $z$, we have $z^T z = \sum_i z_i^2$:

\[\frac{1}{2}(X\theta - \vec{y})^T(X\theta - \vec{y}) = \frac{1}{2}\sum_{i=1}^{n}(h_\theta(x^{(i)}) - y^{(i)})^2 = J(\theta)\]# Demonstrate the matrix formulation

print("Matrix Formulation of Linear Regression")

print("=" * 40)

print(f"Design matrix X shape: {X_single.shape}")

print(f"Target vector y shape: {prices.shape}")

print(f"Parameter vector theta shape: {theta_denorm.shape}")

print("\nFirst 5 rows of design matrix X:")

print(X_single[:5])

print("\nFirst 5 elements of target vector y:")

print(prices[:5])

# Verify the matrix computation

X_theta = X_single @ theta_denorm

residuals = X_theta - prices

print(f"\nX*theta - y (residuals):")

print(f"First 5 residuals: {residuals[:5]}")

# Verify cost computation

cost_matrix = 0.5 * np.dot(residuals, residuals) / len(prices)

cost_function_result = cost_function(X_single, prices, theta_denorm)

print(f"\nCost using matrix formulation: {cost_matrix:.6f}")

print(f"Cost using function: {cost_function_result:.6f}")

print(f"Difference: {abs(cost_matrix - cost_function_result):.10f}")

Matrix Formulation of Linear Regression

========================================

Design matrix X shape: (30, 2)

Target vector y shape: (30,)

Parameter vector theta shape: (2,)

First 5 rows of design matrix X:

[[1.000e+00 2.104e+03]

[1.000e+00 1.600e+03]

[1.000e+00 2.400e+03]

[1.000e+00 1.416e+03]

[1.000e+00 3.000e+03]]

First 5 elements of target vector y:

[400 330 369 232 540]

X*theta - y (residuals):

First 5 residuals: [-39.47813548 -62.44308985 46.12032978 1.61732363 -14.20710549]

Cost using matrix formulation: 693.994731

Cost using function: 693.994731

Difference: 0.0000000000

4.3 Deriving the Normal Equations

To minimize $J$, let’s find its derivatives with respect to $\theta$:

\[\nabla_\theta J(\theta) = \nabla_\theta \frac{1}{2}(X\theta - \vec{y})^T(X\theta - \vec{y})\]Expanding the expression: \(\frac{1}{2}(X\theta - \vec{y})^T(X\theta - \vec{y}) = \frac{1}{2}\left[\theta^T(X^TX)\theta - 2(X^T\vec{y})^T\theta + \vec{y}^T\vec{y}\right]\)

Taking the gradient: \(\nabla_\theta J(\theta) = \frac{1}{2}\left[2X^TX\theta - 2X^T\vec{y}\right] = X^TX\theta - X^T\vec{y}\)

Setting this to zero gives us the normal equations: \(X^TX\theta = X^T\vec{y}\)

Therefore, the value of $\theta$ that minimizes $J(\theta)$ is: \(\theta = (X^TX)^{-1}X^T\vec{y}\)

Matrix Derivative Rules Used:

- $\nabla_x b^T x = b$

- $\nabla_x x^T A x = 2Ax$ (for symmetric matrix $A$)

- $(a^T b) = (b^T a)$ (scalar transpose property)

def normal_equations(X, y):

"""

Solve linear regression using normal equations

Args:

X: Feature matrix (n_samples, n_features)

y: Target vector (n_samples,)

Returns:

theta: Optimal parameters

"""

XTX = X.T @ X

XTy = X.T @ y

# Check if XTX is invertible

if np.linalg.det(XTX) < 1e-10:

print("Warning: X^T X may be singular (not invertible)")

# Use pseudoinverse instead

theta = np.linalg.pinv(XTX) @ XTy

else:

theta = np.linalg.solve(XTX, XTy)

return theta

# Solve using normal equations

print("Normal Equations Solution")

print("=" * 25)

theta_normal = normal_equations(X_single, prices)

cost_normal = cost_function(X_single, prices, theta_normal)

print(f"Normal equations theta: {theta_normal}")

print(f"Normal equations cost: {cost_normal:.6f}")

print("\nComparison with gradient descent:")

print(f"Gradient descent theta: {theta_denorm}")

print(f"Gradient descent cost: {cost_function(X_single, prices, theta_denorm):.6f}")

print(f"\nParameter difference: {np.abs(theta_normal - theta_denorm)}")

print(f"Cost difference: {abs(cost_normal - cost_function(X_single, prices, theta_denorm)):.8f}")

Normal Equations Solution

=========================

Normal equations theta: [-27.75227498 0.18567424]

Normal equations cost: 690.873668

Comparison with gradient descent:

Gradient descent theta: [-27.56992913 0.18445427]

Gradient descent cost: 693.994731

Parameter difference: [0.18234585 0.00121997]

Cost difference: 3.12106359

# Demonstrate with multi-feature dataset

print("Multi-Feature Normal Equations")

print("=" * 30)

theta_multi_normal = normal_equations(X_multi, prices)

cost_multi_normal = cost_function(X_multi, prices, theta_multi_normal)

print(f"Multi-feature parameters: {theta_multi_normal}")

print(f"Multi-feature cost: {cost_multi_normal:.6f}")

# Compare with single feature

print(f"\nModel improvement:")

print(f"Single feature cost: {cost_normal:.6f}")

print(f"Multi-feature cost: {cost_multi_normal:.6f}")

improvement = ((cost_normal - cost_multi_normal) / cost_normal) * 100

print(f"Cost reduction: {improvement:.1f}%")

# Interpret the model

print(f"\nModel interpretation:")

print(f"h(x) = {theta_multi_normal[0]:.2f} + {theta_multi_normal[1]:.6f} * living_area + {theta_multi_normal[2]:.2f} * bedrooms")

print(f"\nMeaning:")

print(f"- Base price: ${theta_multi_normal[0]:.0f}k")

print(f"- Price per sq ft: ${theta_multi_normal[1]*1000:.2f}")

print(f"- Price per bedroom: ${theta_multi_normal[2]:.0f}k")

Multi-Feature Normal Equations

==============================

Multi-feature parameters: [-34.38709557 0.14972143 27.3651073 ]

Multi-feature cost: 623.983673

Model improvement:

Single feature cost: 690.873668

Multi-feature cost: 623.983673

Cost reduction: 9.7%

Model interpretation:

h(x) = -34.39 + 0.149721 * living_area + 27.37 * bedrooms

Meaning:

- Base price: $-34k

- Price per sq ft: $149.72

- Price per bedroom: $27k

# Performance comparison: Gradient Descent vs Normal Equations

import time

print("Performance Comparison")

print("=" * 25)

# Generate a larger dataset for timing

np.random.seed(42)

n_large = 1000

n_features = 10

X_large = np.random.randn(n_large, n_features)

X_large = np.column_stack([np.ones(n_large), X_large]) # Add intercept

true_theta = np.random.randn(n_features + 1)

y_large = X_large @ true_theta + 0.1 * np.random.randn(n_large)

print(f"Large dataset: {n_large} samples, {n_features} features")

# Time normal equations

start_time = time.time()

theta_normal_large = normal_equations(X_large, y_large)

normal_time = time.time() - start_time

# Time gradient descent (with normalization)

X_large_norm, mu_large, sigma_large = normalize_features(X_large)

start_time = time.time()

theta_gd_large, _, _ = batch_gradient_descent(

X_large_norm, y_large, alpha=0.01, num_iterations=1000

)

theta_gd_large = denormalize_theta(theta_gd_large, mu_large, sigma_large)

gd_time = time.time() - start_time

print(f"\nTiming results:")

print(f"Normal Equations: {normal_time:.4f} seconds")

print(f"Gradient Descent: {gd_time:.4f} seconds")

print(f"Speedup: {gd_time/normal_time:.1f}x faster with Normal Equations")

# Compare accuracy

cost_normal_large = cost_function(X_large, y_large, theta_normal_large)

cost_gd_large = cost_function(X_large, y_large, theta_gd_large)

print(f"\nAccuracy comparison:")

print(f"Normal Equations cost: {cost_normal_large:.8f}")

print(f"Gradient Descent cost: {cost_gd_large:.8f}")

print(f"Parameter difference (L2 norm): {np.linalg.norm(theta_normal_large - theta_gd_large):.8f}")

print(f"\n{'Method':<20} {'Features < 1000':<15} {'Features > 10000':<15}")

print("-" * 50)

print(f"{'Gradient Descent':<20} {'✓':<15} {'✓ (preferred)':<15}")

print(f"{'Normal Equations':<20} {'✓ (preferred)':<15} {'✗ (too slow)':<15}")

Performance Comparison

=========================

Large dataset: 1000 samples, 10 features

Iteration 0: Cost = 3.7232, theta = [-0.0078457 -0.0031994 -0.00668323 0.00119587 0.01287764 -0.00791111

0.01099471 -0.00904892 -0.00839605 0.00901522 0.00956148]

Iteration 100: Cost = 0.4436, theta = [-0.50026406 -0.19987003 -0.41011996 0.07316454 0.78919657 -0.50235488

0.68226504 -0.54815696 -0.54535291 0.54844182 0.58660277]

Iteration 200: Cost = 0.0571, theta = [-0.6805051 -0.26894044 -0.54378114 0.09654439 1.04767793 -0.68135116

0.91288516 -0.72258678 -0.74987391 0.72455761 0.77906625]

Iteration 300: Cost = 0.0110, theta = [-0.74647915 -0.29351987 -0.58749983 0.10386678 1.13397745 -0.7460469

0.99242638 -0.77917968 -0.8273209 0.78200897 0.84330981]

Iteration 400: Cost = 0.0054, theta = [-0.77062779 -0.30238201 -0.60156795 0.10604867 1.16288467 -0.76939732

1.01996988 -0.79760881 -0.85652548 0.80071056 0.86476506]

Iteration 500: Cost = 0.0048, theta = [-0.77946697 -0.3056183 -0.60599789 0.10665079 1.17260584 -0.77781432

1.0295463 -0.80363939 -0.86750662 0.80677442 0.87193154]

Iteration 600: Cost = 0.0047, theta = [-0.7827024 -0.30681466 -0.60735132 0.10679495 1.1758907 -0.78084467

1.03288948 -0.80562526 -0.87162816 0.80872789 0.87432454]

Iteration 700: Cost = 0.0047, theta = [-0.78388667 -0.30726205 -0.6077466 0.10681849 1.1770072 -0.78193436

1.03406136 -0.80628446 -0.87317371 0.80935084 0.87512286]

Iteration 800: Cost = 0.0047, theta = [-0.78432015 -0.30743117 -0.60785376 0.10681601 1.17738942 -0.78232572

1.03447381 -0.80650547 -0.87375321 0.80954642 0.87538872]

Iteration 900: Cost = 0.0047, theta = [-0.78447882 -0.30749574 -0.60787887 0.10681092 1.17752139 -0.78246608

1.03461955 -0.80658047 -0.87397061 0.80960635 0.87547701]

Timing results:

Normal Equations: 0.0004 seconds

Gradient Descent: 0.0771 seconds

Speedup: 199.8x faster with Normal Equations

Accuracy comparison:

Normal Equations cost: 0.00467521

Gradient Descent cost: 0.00467521

Parameter difference (L2 norm): 0.00007954

Method Features < 1000 Features > 10000

--------------------------------------------------

Gradient Descent ✓ ✓ (preferred)

Normal Equations ✓ (preferred) ✗ (too slow)

5. Section 1.3: Probabilistic Interpretation

When faced with a regression problem, why might linear regression, and specifically why might the least-squares cost function $J$, be a reasonable choice?

In this section, we will give a set of probabilistic assumptions under which least-squares regression is derived as a very natural algorithm.

5.1 Probabilistic Model

Let us assume that the target variables and inputs are related via the equation: \(y^{(i)} = \theta^T x^{(i)} + \epsilon^{(i)}\)

where $\epsilon^{(i)}$ is an error term that captures:

- Unmodeled effects (features we didn’t include)

- Random noise

Key Assumptions:

- The errors $\epsilon^{(i)}$ are independently and identically distributed (IID)

- The errors follow a Gaussian (normal) distribution: $\epsilon^{(i)} \sim \mathcal{N}(0, \sigma^2)$

This implies: \(y^{(i)} | x^{(i)}; \theta \sim \mathcal{N}(\theta^T x^{(i)}, \sigma^2)\)

In other words, given $x^{(i)}$ and $\theta$, $y^{(i)}$ follows a normal distribution with mean $\theta^T x^{(i)}$ and variance $\sigma^2$.

# Demonstrate the probabilistic interpretation

print("Probabilistic Interpretation of Linear Regression")

print("=" * 50)

# Use our fitted model to demonstrate the concepts

predictions = linear_hypothesis(X_single, theta_normal)

residuals = prices - predictions

sigma_estimate = np.std(residuals)

print(f"Estimated noise standard deviation: σ = {sigma_estimate:.2f}")

print(f"Mean of residuals: {np.mean(residuals):.4f} (should be ≈ 0)")

# Test if residuals are approximately normally distributed

from scipy import stats

# Shapiro-Wilk test for normality

statistic, p_value = stats.shapiro(residuals)

print(f"\nNormality test (Shapiro-Wilk):")

print(f"Statistic: {statistic:.4f}, p-value: {p_value:.4f}")

print(f"Residuals are {'approximately normal' if p_value > 0.05 else 'not normal'} (α = 0.05)")

# Visualize the probabilistic model

fig, axes = plt.subplots(2, 2, figsize=(15, 10))

# Plot 1: Data with uncertainty bands

axes[0, 0].scatter(living_areas, prices, alpha=0.7, s=60, color='blue', label='Data')

x_line = np.linspace(living_areas.min(), living_areas.max(), 100)

y_line = theta_normal[0] + theta_normal[1] * x_line

axes[0, 0].plot(x_line, y_line, 'r-', linewidth=2, label='Mean prediction')

# Add uncertainty bands (±1σ and ±2σ)

axes[0, 0].fill_between(x_line, y_line - sigma_estimate, y_line + sigma_estimate,

alpha=0.3, color='red', label='±1σ band')

axes[0, 0].fill_between(x_line, y_line - 2*sigma_estimate, y_line + 2*sigma_estimate,

alpha=0.15, color='red', label='±2σ band')

axes[0, 0].set_xlabel('Living Area (sq ft)')

axes[0, 0].set_ylabel('Price (1000$s)')

axes[0, 0].set_title('Probabilistic Model with Uncertainty')

axes[0, 0].legend()

axes[0, 0].grid(True, alpha=0.3)

# Plot 2: Residuals histogram

axes[0, 1].hist(residuals, bins=15, alpha=0.7, color='green', edgecolor='black', density=True)

# Overlay theoretical normal distribution

x_norm = np.linspace(residuals.min(), residuals.max(), 100)

y_norm = stats.norm.pdf(x_norm, np.mean(residuals), sigma_estimate)

axes[0, 1].plot(x_norm, y_norm, 'r-', linewidth=2, label=f'N(0, {sigma_estimate:.1f}²)')

axes[0, 1].set_xlabel('Residuals')

axes[0, 1].set_ylabel('Density')

axes[0, 1].set_title('Distribution of Residuals')

axes[0, 1].legend()

axes[0, 1].grid(True, alpha=0.3)

# Plot 3: Q-Q plot for normality

stats.probplot(residuals, dist="norm", plot=axes[1, 0])

axes[1, 0].set_title('Q-Q Plot (Normal Distribution)')

axes[1, 0].grid(True, alpha=0.3)

# Plot 4: Residuals vs fitted values

axes[1, 1].scatter(predictions, residuals, alpha=0.7, s=60, color='purple')

axes[1, 1].axhline(y=0, color='red', linestyle='--', alpha=0.7)

axes[1, 1].set_xlabel('Fitted Values')

axes[1, 1].set_ylabel('Residuals')

axes[1, 1].set_title('Residuals vs Fitted Values')

axes[1, 1].grid(True, alpha=0.3)

plt.tight_layout()

plt.show()

Probabilistic Interpretation of Linear Regression

==================================================

Estimated noise standard deviation: σ = 37.17

Mean of residuals: -0.0000 (should be ≈ 0)

Normality test (Shapiro-Wilk):

Statistic: 0.9809, p-value: 0.8481

Residuals are approximately normal (α = 0.05)

5.2 Maximum Likelihood Estimation

Given our probabilistic model, we can derive the least squares cost function using maximum likelihood estimation.

The likelihood of the parameters given the data is: \(L(\theta) = \prod_{i=1}^{n} p(y^{(i)} | x^{(i)}; \theta)\)

| Since $y^{(i)} | x^{(i)}; \theta \sim \mathcal{N}(\theta^T x^{(i)}, \sigma^2)$: |

Therefore: \(L(\theta) = \prod_{i=1}^{n} \frac{1}{\sqrt{2\pi}\sigma} \exp\left(-\frac{(y^{(i)} - \theta^T x^{(i)})^2}{2\sigma^2}\right)\)

The log-likelihood is: \(\ell(\theta) = \log L(\theta) = n\log\frac{1}{\sqrt{2\pi}\sigma} - \frac{1}{2\sigma^2} \sum_{i=1}^{n} (y^{(i)} - \theta^T x^{(i)})^2\)

Maximizing the log-likelihood is equivalent to minimizing: \(\frac{1}{2} \sum_{i=1}^{n} (y^{(i)} - \theta^T x^{(i)})^2\)

This is exactly our least squares cost function $J(\theta)$!

def log_likelihood(theta, X, y, sigma):

"""

Compute log-likelihood for linear regression with Gaussian noise

Args:

theta: Parameter vector

X: Feature matrix

y: Target vector

sigma: Noise standard deviation

Returns:

log_likelihood: Log-likelihood value

"""

n = len(y)

predictions = linear_hypothesis(X, theta)

residuals_sq = (y - predictions) ** 2

log_lik = n * np.log(1 / (np.sqrt(2 * np.pi) * sigma)) - (1 / (2 * sigma**2)) * np.sum(residuals_sq)

return log_lik

def negative_log_likelihood(theta, X, y, sigma):

"""Negative log-likelihood (for minimization)"""

return -log_likelihood(theta, X, y, sigma)

# Demonstrate the connection between MLE and least squares

print("Maximum Likelihood Estimation Connection")

print("=" * 40)

# Compute log-likelihood for our solution

log_lik = log_likelihood(theta_normal, X_single, prices, sigma_estimate)

print(f"Log-likelihood at optimal theta: {log_lik:.2f}")

# Show that minimizing negative log-likelihood gives same result as least squares

from scipy.optimize import minimize

# Optimize using negative log-likelihood

result = minimize(negative_log_likelihood,

x0=np.array([0, 0]),

args=(X_single, prices, sigma_estimate),

method='BFGS')

theta_mle = result.x

print(f"\nMLE solution: {theta_mle}")

print(f"Normal equations: {theta_normal}")

print(f"Difference: {np.abs(theta_mle - theta_normal)}")

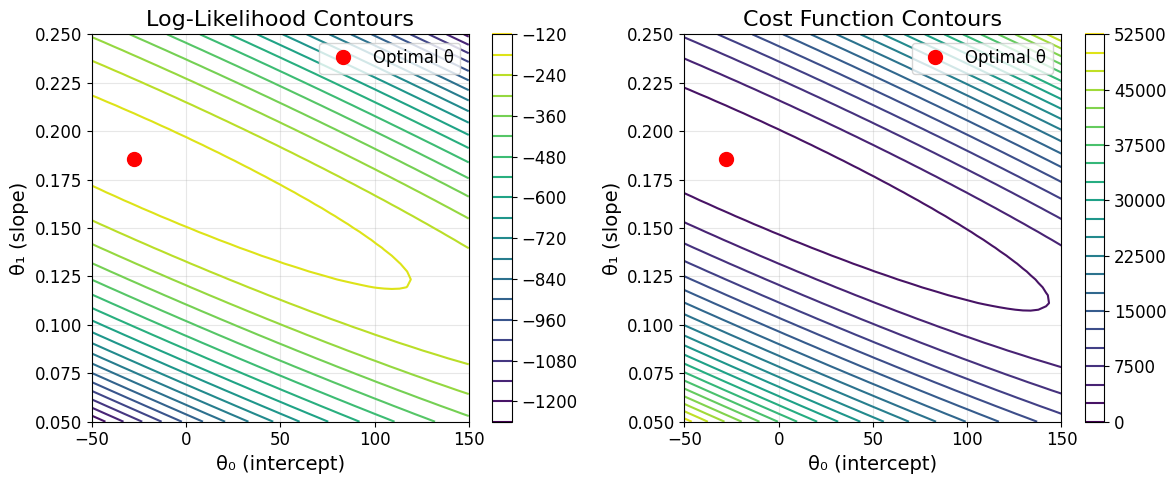

# Visualize likelihood surface

theta0_range = np.linspace(-50, 150, 50)

theta1_range = np.linspace(0.05, 0.25, 50)

THETA0, THETA1 = np.meshgrid(theta0_range, theta1_range)

LOG_LIK = np.zeros_like(THETA0)

for i in range(len(theta0_range)):

for j in range(len(theta1_range)):

theta_test = np.array([THETA0[j, i], THETA1[j, i]])

LOG_LIK[j, i] = log_likelihood(theta_test, X_single, prices, sigma_estimate)

plt.figure(figsize=(12, 5))

plt.subplot(1, 2, 1)

contour = plt.contour(THETA0, THETA1, LOG_LIK, levels=20)

plt.plot(theta_normal[0], theta_normal[1], 'ro', markersize=10, label='Optimal θ')

plt.xlabel('θ₀ (intercept)')

plt.ylabel('θ₁ (slope)')

plt.title('Log-Likelihood Contours')

plt.legend()

plt.colorbar(contour)

plt.grid(True, alpha=0.3)

plt.subplot(1, 2, 2)

# Show equivalent cost function contours

COST = np.zeros_like(THETA0)

for i in range(len(theta0_range)):

for j in range(len(theta1_range)):

theta_test = np.array([THETA0[j, i], THETA1[j, i]])

COST[j, i] = cost_function(X_single, prices, theta_test)

contour2 = plt.contour(THETA0, THETA1, COST, levels=20)

plt.plot(theta_normal[0], theta_normal[1], 'ro', markersize=10, label='Optimal θ')

plt.xlabel('θ₀ (intercept)')

plt.ylabel('θ₁ (slope)')

plt.title('Cost Function Contours')

plt.legend()

plt.colorbar(contour2)

plt.grid(True, alpha=0.3)

plt.tight_layout()

plt.show()

print("\nKey insight: Maximizing likelihood ≡ Minimizing least squares cost")

print("This justifies the choice of least squares from a probabilistic perspective!")

Maximum Likelihood Estimation Connection

========================================

Log-likelihood at optimal theta: -151.03

MLE solution: [-27.75140262 0.18567386]

Normal equations: [-27.75227498 0.18567424]

Difference: [8.72353017e-04 3.80915347e-07]

Key insight: Maximizing likelihood ≡ Minimizing least squares cost

This justifies the choice of least squares from a probabilistic perspective!

Summary and Key Takeaways

What We’ve Learned

1. Supervised Learning Framework

- Goal: Learn a hypothesis function $h: \mathcal{X} \mapsto \mathcal{Y}$

- Components: Training examples $(x^{(i)}, y^{(i)})$, features, targets

- Types: Regression (continuous $y$) vs Classification (discrete $y$)

2. Linear Regression Model

- Hypothesis: $h_\theta(x) = \theta^T x = \theta_0 + \theta_1 x_1 + \cdots + \theta_d x_d$

- Cost Function: $J(\theta) = \frac{1}{2} \sum_{i=1}^{n} (h_\theta(x^{(i)}) - y^{(i)})^2$

- Properties: Convex optimization, unique global minimum

3. Optimization Methods

Gradient Descent (LMS Algorithm)

- Update Rule: $\theta_j := \theta_j - \alpha \frac{\partial}{\partial \theta_j} J(\theta)$

- Batch GD: Uses all examples per update

- Stochastic GD: Uses one example per update, faster for large datasets

- Key: Requires feature normalization for good performance

Normal Equations

- Closed-form: $\theta = (X^T X)^{-1} X^T \vec{y}$

- Advantages: Exact solution, no iterations, no learning rate

- Disadvantages: $O(d^3)$ complexity, memory intensive for large $d$

4. Probabilistic Justification

- Model: $y^{(i)} = \theta^T x^{(i)} + \epsilon^{(i)}$ where $\epsilon^{(i)} \sim \mathcal{N}(0, \sigma^2)$

- Maximum Likelihood Estimation leads naturally to least squares cost function

- Provides theoretical foundation for linear regression

5. Practical Guidelines

| Scenario | Recommended Method | Notes |

|---|---|---|

| Small datasets ($n < 1000, d < 100$) | Normal Equations | Fast, exact |

| Medium datasets ($d < 1000$) | Either method | Normal equations often faster |

| Large datasets ($d > 1000$ or $n > 10^6$) | Gradient Descent | Scalable, memory efficient |

| Online learning | Stochastic GD | Can adapt to new data |

Implementation Checklist

- Data preprocessing: Handle missing values, outliers

- Feature normalization: Essential for gradient descent

- Parameter initialization: Start with zeros or small random values

- Learning rate tuning: Start with 0.01, adjust based on convergence

- Convergence monitoring: Track cost function, check for oscillations

- Model validation: Check residuals, test normality assumptions

Next Steps

This foundation in linear regression enables understanding of:

- Regularization (Ridge, Lasso regression)

- Logistic regression for classification

- Neural networks as extensions of linear models

- Advanced optimization methods (Adam, RMSprop)